Debt Financing as a Structural Shield: Capital Intensity, CSR, and Tax Aggressiveness in Indonesian Manufacturing

DOI:

https://doi.org/10.63924/jsid.v8i1.305Keywords:

Capital Intensity, Leverage, Corporate Social Responsibility, Tax Aggressiveness, Manufacturing FirmsAbstract

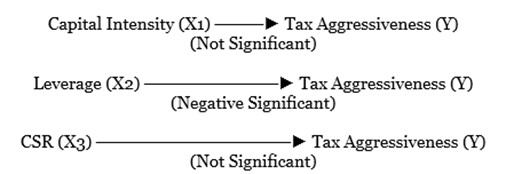

Tax aggressiveness remains a persistent concern for fiscal authorities and stakeholders, as it directly diminishes public revenue and complicates regulatory compliance. While firm-level attributes such as capital intensity, leverage, and corporate social responsibility (CSR) frequently inform discussions on tax planning, empirical consensus regarding their influence remains elusive, particularly within the Indonesian manufacturing sector. This study investigates the impact of these three determinants on corporate tax aggressiveness among manufacturing entities listed on the Indonesia Stock Exchange (IDX). Utilizing a quantitative framework, we applied panel data regression analysis to a purposive sample of 93 manufacturing firms observed between 2019 and 2024. Our analysis reveals that neither capital intensity nor CSR exerts a statistically significant influence on tax aggressiveness. Conversely, leverage demonstrates a significant negative association with tax aggressive behavior. This inverse relationship suggests that firms maintaining higher debt levels benefit from substantial interest tax shields; these deductible expenses effectively lower taxable income, thereby reducing the firm's overall tax liability. These findings indicate that leverage serves as a primary mechanism for tax management in this context. Rather than pursuing aggressive avoidance strategies, highly leveraged firms appear to prioritize the inherent tax advantages derived from their financing structures. These results offer critical implications for policymakers, investors, and corporate managers navigating the intersection of capital structure decisions and fiscal compliance.

References

Ami, A., & Lindawati, L. (2024). The Effect of Corporate Social Responsibility and Good Corporate Governance on Earnings Management. EKOMA: Journal of Economics, Management, and Accounting, 3(6), 933–943. https://doi.org/10.56799/ekoma.v3i6.510

Apriliana, N. (2022). The effect of liquidity, profitability, and leverage on tax aggressiveness. Journal of Financial Scholars, 1(1). https://doi.org/10.32503/jck.v1i1.2239

Apriyanti, HW, & Arifin, M. (2021). Determinants of Tax Aggressiveness. Journal of Islamic Accounting and Finance Research, 3(1), 27–52. https://doi.org/10.21580/jiafr.2021.3.1.7412

Burhanudin, & Kodriyah. (2023). The Effect of Profitability and Leverage on Tax Aggressiveness. Journal of Management Accounting (JAKMEN), 2(1), 30–49. https://doi.org/10.30656/jakmen.v2i1.6926

Dwiyanti, IAI, & Jati, IK (2019). The Effect of Profitability, Capital Intensity, and Inventory Intensity on Tax Avoidance. Electronic Journal of Accounting, 27, 2293. https://doi.org/10.24843/eja.2019.v27.i03.p24

Kogha, VR, & Nursyirwan, VI (2021). The Effect of Inventory Intensity, Capital Intensity, and Corporate Social Responsibility on Tax Management. Sakuntala, 1(1). http://openjournal.unpam.ac.id/index.php/SAKUNTALA

Kusumawati, A., Kartika, A., & Akuntansi, J. (2023). The Effect of Leverage and Capital Intensity on Tax Aggressiveness in Profitability as a Moderation. Scientific Journal of Accounting Students) Ganesha University of Education, 14, 2.

Malik, A., Pratiwi, A., & Umdiana, N. (2022). The Effect of Company Size, Sales Growth, and Capital Intensity on Tax Avoidance. “LAWSUIT” Taxation Journal, 1(2), 92–108. https://doi.org/10.30656/lawsuit.v1i2.5552

Muliawati, IAPY, & Karyada, IPF (2021). Hita Accounting and Finance, Hindu University of Indonesia, January 2021 Edition. Journal of the Faculty of Economics, Business and Tourism, Hindu University of Indonesia, 1–25.

Noerhafizah, L., Supriyanto, J., & Fadillah, H. (2024). The Effect of Profitability, Liquidity, and Leverage on Tax Aggressiveness in Coal Mining Companies Listed on the Indonesia Stock Exchange in 2017-2021. Jurnal Akuntansi Pratama, Vol. 1 No. (2), 1–13.

Puteri, NC (2024). The Effect of Audit Committee and Capital Intensity on Tax Aggressiveness. Indonesian Journal of Management Studies, 2(3), 1–10. https://doi.org/10.53769/ijms.v2i3.582

Putri, AA, & Hanif, RA (2020). The Effect of Liquidity, Leverage, and Audit Committee on Tax Aggressiveness. Current: Journal of Current Accounting and Business Studies, 1(3). https://doi.org/10.31258/jc.1.3.384-401

Rahayu, U., & Kartika, A. (2021). The Effect of Profitability, Corporate Social Responsibility, Capital Intensity, and Company Size on Tax Aggressiveness. Jurnal Maneksi, 10(1), 25–33. https://doi.org/10.31959/jm.v10i1.635

Rahmadi, ZT, & Suharti, E. (2018). The Effect of Capital Intensity and Leverage on Tax Aggressiveness in Manufacturing Companies Listed on the Indonesia Stock Exchange (IDX) Period 58–73.

Ramadani, DC, & Hartiyah, S. (2020). The Influence of Corporate Social Responsibility, Leverage, Liquidity, Company Size, and Independent Commissioners on Tax Aggressiveness (Empirical Study of Mining Companies Listed on the Indonesia Stock Exchange from 2014 to 2018). Journal of Economics, Business, and Engineering (JEBE), 1(2). https://doi.org/10.32500/jebe.v1i2.1219

Riswandari, E., & Bagaskara, K. (2020). Tax Aggressiveness Influenced by Executive Compensation, Political Connections, Sales Growth, Leverage, and Profitability. Journal of Accounting, 10(3), 261–274. https://doi.org/10.33369/j.akuntansi.10.3.261-274

Saifuddin Azwar. (2011). Human Attitude: Theory and Measurement (2nd Ed., 2nd Edition). Student Library.

Soelistiono, S., & Adi, PH (2022). The Effect of Leverage, Capital Intensity, and Corporate Social Responsibility on Tax Aggressiveness. Journal of Modern Economics, 18(1), 38–51. https://doi.org/10.21067/jem.v18i1.6260

Wijaya, D. (2019). The Effect of Corporate Social Responsibility Disclosure, Leverage, and Managerial Ownership on Tax Aggressiveness. Widyakala Journal, 6(1). https://doi.org/10.36262/widyakala.v6i1.147

Yahya, A., Agustin, EG, & Nurastuti, P. (2022). Firm Size, Capital Intensity, and Inventory Intensity on Tax Aggressiveness. Journal of Accounting Exploration, 4(3), 574–588. https://doi.org/10.24036/jea.v4i3.615

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Nur Afni Yunita, Muhammad Yusra, Sri Mulyati, Fitri Maghfirah

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

.png)

%20(4).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)